The case for infrastructure pricing reform - What water can teach roads

Chairman's speech

Peter Harris delivered a speech to the Infrastructure Partners Australia Water Symposium in Sydney on 27 July 2015.

Download the speech

Read the speech

The Productivity Commission has had the chance to do two major studies in recent years into probably the two most controversial areas of infrastructure: roads and water.

And other bodies too, the Commission of Audit and the recent Harper Review of competition policy, have also found these two reform areas to be worthy of serious attention.

Mind you, these are the most controversial topics in infrastructure probably only if we assume that electricity pricing is now stable, after itself suffering major upset due to misjudging infrastructure needs; and some poor practice in the pricing sphere.

Life's never dull in infrastructure.

Most of the major suppliers of infrastructure work in a price-regulated industry.

Water, gas, electricity, telecommunications all have substantial pricing regimes and even occasionally have policy updates applied to them. Increasingly, consumer interests - demand and quality of service, for example - are more directly being taken into account by each of these.

What this means for those who believe in markets offering at least some guiding principles for efficient resource allocation in a regulated industry, is that consumer willingness to pay is being given at least a modicum of recognition.

Not so in roads.

The assumption is still if you build it, they will pay …or have already paid, depending on which school you went to.

And moreover, who precisely 'they' is, can be quite remote:

- Remote from the actual users of the road.

- Remote from the decision to build the thing in the first place.

In water or most other infrastructure, user pays is a very well-recognised subject. Not so well developed that it cannot be significantly improved, but there as foundation. Not in roads.

I will return to roads at the end of this address, as that is where the biggest bang for buck lies in infrastructure reform. And it would be remiss of me to not continue the argument in favour of road reform, even at a water conference.

But, first, water.

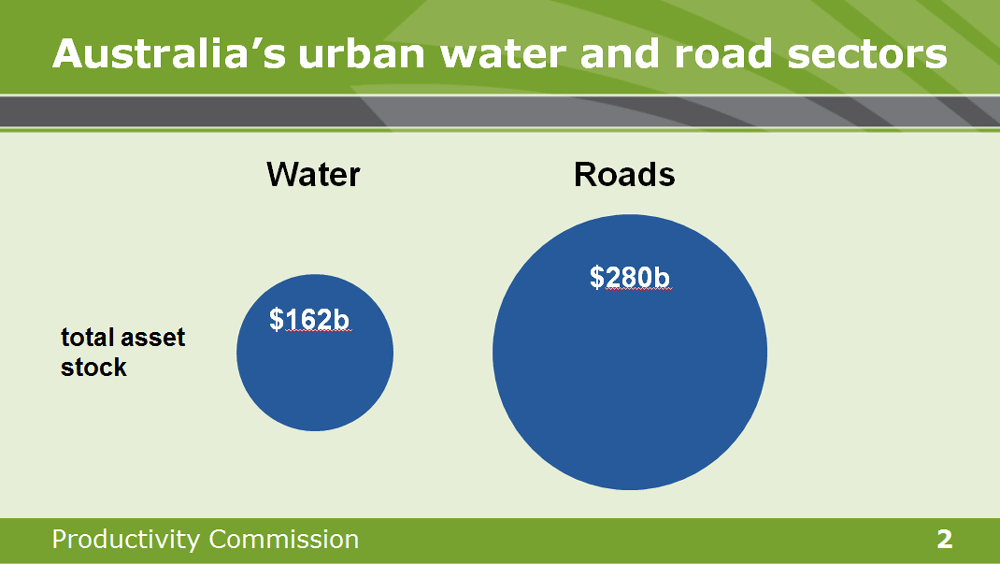

The current regulated asset base in urban water is worth approximately $160 billion. In total, planned capital expenditure in 2013 is about $5bn. Not trivial, but not of the scale of the investment process we went through in 2000s.

And productivity in the water sector was seriously impaired during drought years as:

- restrictions on supply meant production fell but labour and capital used did not

- after restrictions proved insufficient (and I won't argue today about why that is, but we could easily fill an hour on that alone) then capital was poured into leaks and seeps investments, and then into insurance-type investments in desalination and recycling.

Productivity has not recovered quickly, even with the end of drought and restrictions, although in very recent times it may be showing some positive growth.

In order to see investment in the urban water sector manage these challenges better in the future, the lessons of the recent past need to be recognised and applied to both the governance structure of the industry and to the regulated pricing arrangements.

In particular, my contention today will be that the urban water sector is able, because of the things that we all learned in the 2000s, to make greater use of consumer information to improve both its investment planning and its pricing structure.

One thing we can say as a consequence of the drought is that all water authorities - and hopefully regulators - learned very useful lessons in how to provide information to consumers in order to influence demand.

We should build on this, not revert to an assumption of ever-increasing demand, with supply increments growing according to past profiles.

That's a different proposition to the usual design issues that are discussed in infrastructure, but I contend that in any investment policy discussion, the consumer is the right place to start.

Here's the rub. Regulated pricing of the cost recovery kind does not really involve consumers much at all. As a rough guide, a supplier develops a capital and recurrent expenditure program; the regulator reviews it against the proponent's stated needs; discount factors are debated and then finally prices are adjusted.

Consumers generally just pay.

There may occasionally be some attention given to recent demand trends but assets are so long-lived that reasonable doubt can always be asserted about the relevance of demand shifts of a recent nature.

And since the costs of getting it wrong are significant, erring on the side of over-provision can occur in even the best regulated structure.

How then can we do better in involving consumers in regulated pricing models? And why should we bother trying?

Let me try to answer the why question first.

In the previous decade (2000-2010), the value of water supply - long taken for granted - became strongly evident to urban communities. All of the East Coast of Australia faced threats to water supply of varying dimensions, threats that Perth had started to face a generation earlier; and that Adelaide had suffered to some degree for many years.

The initial response was an odd mixture of restrictions, forced private provision (in the form of water tanks for lawns and gardens) and encouragement for private provision (in the form of subsidies for internal recycling of water).

But as these became less convincing, big capital projects replaced them.

The alternative - variation in the price of water to reflect scarcity - was a nice theoretical concept. But since the cost recovery approach to pricing requires a cost to be incurred - or at least a provision for one - before a price moves, the idea was out of sync with the regulatory structure. So the scope to vary price to reflect scarcity was absent.

And the value of action - in the form of large projects - was also politically very attractive.

Whereas even the smallest attempt to raise price for large users via a two-part tariff was quite fraught for some politicians.

Even after this was eventually applied in some jurisdictions, the price structure of the average user's bill says in effect:

- the water's cheap, but that supply system is really expensive.

My bills say that, today. And I pay water bills in two East Coast States and have lived in another during this reform period.

Of course, as a consumer I can save one but not the other; so price isn't encouraging me to be more efficient.

Or to indicate what demand might genuinely be.

It's suggested that water use is inelastic, and that scarcity pricing may have no effect.

Yet studies conducted here, in Sydney, on water use during the drought do show that price had a desirable effect on demand, after controlling for other factors as far as possible, even though those price shifts were not created via scarcity pricing.

And we also know through more indirect means that consumers are not impervious to forms of price incentive, to reduce water use.

The encouragement to invest privately in home water systems - rainwater tanks and revised plumbing systems - was accepted by some during the drought years.

Admittedly, the price signal was extraordinary: four or five times the metered cost per kilolitre, for an average suburban house.

Whereas a revised pricing structure that merely allowed consumers to recognise the options - a choice between long-term cost increase due to major new supply options, versus short-term price rises until inflow patterns return to something approaching normal would offer us all the chance to be more efficient and apply something more akin to market principles.

The effectiveness of current billing for cost recovery as an objective is not in doubt. The effectiveness of billing for creating choices in future supply, a better objective, is.

In our 2011 Report on Urban Water, we proposed significant changes to governance structures to also improve the judgments made on water investment.

In part, these governance changes were intended to allow water supply options (including serious price reform) to be developed that reflect the most efficient sources of supply, rather than to see options ruled out by community perception, and the response of politicians to it.

This can easily be misinterpreted to imply that there is no role for governments to rule in or out particular projects. It can never mean that.

But the governance structure for water needs to evolve, as it has for electricity or airports or even rail today, to the point that the data on the relative costs of the full range of supply options is on the table before any political action is taken to rule an option out.

You need to know what you're giving up, before you give it up.

Some of you may be wondering why I am talking today about reform options when we don't have much need of major supply options today.

We have desalination plants in reserve and dams are pretty full in many cases. Recycling too is more easily triggered, today, for some non-potable purposes.

So why bother?

The answer to that lies with climate change. Any rational supplier of water needs to develop scenario planning that allows for the possibility of a serious loss of rainfall as an increasing likelihood.

How likely? Of course, we don't know. Climate models are probably not really that useful for such forecasting, which is why I referred to scenarios.

But if we have clearer accountability in the decision-making, and if we have options to put in front of consumers that allow price to be considered as a response, rather than as a consequence of a big investment, then unlike the start of the 2000s drought sequence, we achieve that rare event in public policy - a user-driven model.

And to allow these choices to be developed, governance structures - that of the regulators and that of the water supply businesses - should be changed.

Pricing regulators should be given greater ability to consider - to weigh up, transparently - what can be achieved by a variety of options, not just remain tied to cost recovery.

In an environment of constant demand growth, cost recovery may work adequately. But it may be an invalid assumption for some infrastructure industries, as electricity has shown.

And it will improve our productivity if we can take the efficiency route and actually gain more value add out of selling less water.

Which is, after all, better productivity. And why I'm here today.

These are some of our largest public investments, at the irregular times they are made.

The consequences remain with us for decades after some of them are made.

Having an inefficient asset base for decades is not just a burden on consumers but at some point if large enough a burden on society. We should not allow our capital investment choices to be so deeply skewed.

And as our 2011 report showed, failing to pursue such options in urban water in two communities alone may have over time very large implications, in excess of a billion dollars.

For those whose interest today stretches solely to water reform, this is the point to duck out for a coffee.

Because much as it is true there is more work to be done in urban water, at least there is a foundation on which to build change.

The situation is more dire in roads. The cycle of building here is not in a downward phase, in fact it is not really a cycle at all; more like a perpetual search for solutions.

And large as water investments are, the road asset base is larger. Getting it wrong has all the larger long term costs.

There are reform processes struggling to break out in roads policy.

Curiously, the private sector is doing more of the leading than the public sector.

Some of you may have heard of the trials now being run in Melbourne by Transurban on electronic road pricing.

Transurban is undertaking a Road Network Pricing Study in Melbourne that will trial various user-pays models in real-world conditions. It is intended to test different pricing models and indicate driver responses. Drivers have been signed up and the results of the trials will be published. This has the capacity to be a serious and useful contribution to the road funding discussion.

Transurban doesn't have to buy into this debate. It already has a tolling technology. It has a growing inventory of assets under management.

But whilst ever the alternative, trials by a public sector agency, are off the agenda, there is scope here to obtain Australian data on ways to make assets operate more efficiently.

And to use price to do it.

For those of you who have resisted the temptation to go for coffee, I hope you will see the commonality with my earlier comments on water: start with consumers, show them the choice of price or cost, gain responses that help you know the real level of demand.

Aside from any private interests of Transurban, the public interest potentially served by this trial is significant.

Not so much in congestion management, which some have seen as the next step.

But rather in the bigger topic of better allocation of road assets, as a contributor to more efficient transport and so to improved productivity as a wide range of user industries.

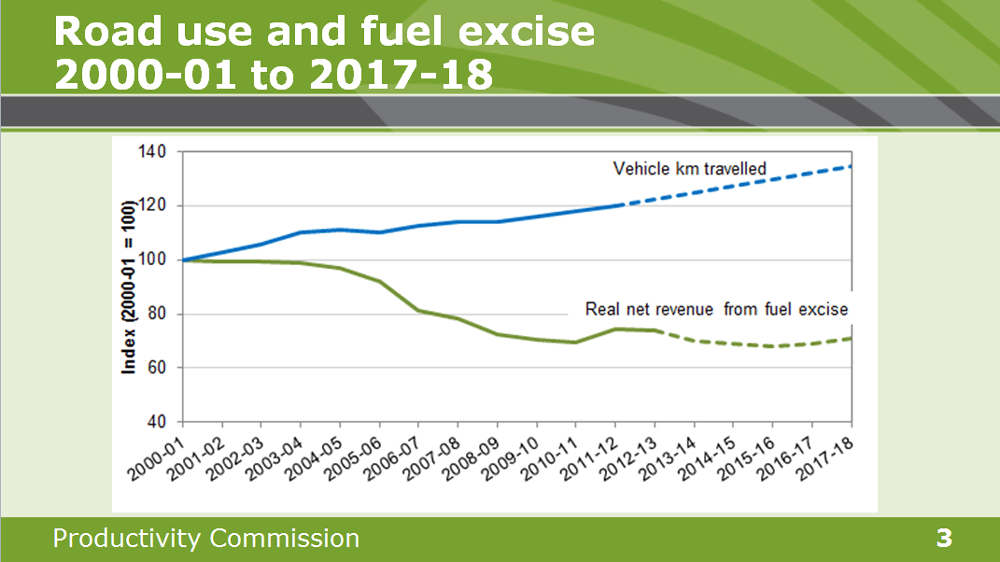

The need for reform to extend beyond congestion is best encapsulated in this graph from our 2014 Infrastructure Report.

Some public policy trials of road user pricing, rather than just congestion pricing, are also being conducted overseas. Oregon is trialing in a manner not too different to Transurban.

Elsewhere in the US, the advent of in-vehicle technology for collision avoidance systems - using signals between one vehicle and another vehicle, and vehicles and monitors designed to reduce pedestrian-related collisions at intersections - is upon us.

The US National Transport Safety Administration is assessing a rule mandating changes to vehicle design for just this purpose.

Like all remarkable technologies, there is no guarantee that we will see it applied - here or even overseas - just because it can be done.

But in-vehicle systems create the opportunity to address this bigger challenge: how do we pay for all the roads we seem to want?

For the first time, there is a plausible mechanism for user pays arrangements in roads.

And a mechanism that can allow the substitution of direct charging for today's poor proxies for road use: fuel excise and registration.

I am not predicting the early application of this technology.

Usually, the transfer from 'it can be done' to 'it's actually happened' takes much longer than any of us imagine. But the technology is not bleeding edge: it's no more sophisticated than most of you have in your pockets today.

Nevertheless, what we should not be doing now is running off to check to technology websites. There are stronger incentives for others to do that.

Similarly to water policy, the essential step now is to get the institutional decision-making structure right.

It will be essential to applying user pays in roads for there to be a system in which consumers have confidence that the substitution over time and location of one charging mechanism for another i.e. how excise and registration give way to direct charging, will work to meet their needs.

If you don't have this, you don't have much at all.

The revised Commonwealth/State structure for this alone will take years to bed down. So best to start soon.

A roads investment structure that will give confidence to motorists and truck owners - let's call them all consumers - must improve major project selection while reducing other forms of charging. It has to project in unmistakable terms that this structure is designed for consumers to choose.

If not, we will see this opportunity pass us by. Simply because if the very important pre-conditions are not in place, it will not matter a damn how much technology is available.

Technology will instead simply be designed solely to motor vehicle rather than road use specifications and at best we will face a twenty-first century replay of the nineteenth century rail gauge issue: multiple systems, none fit for national purpose, an impediment to reform and all with ad hoc and heavily parochial objectives.

These pre-conditions are:

- first, since the current revenue sources are both Federal (i.e. excise) and State (registration charges), a revised structure will need to see both levels of government co-operate and combine their funds for the purposes of project allocation.

A joint funding allocation process for selecting projects, one for each State and Territory, is the right starting point. Although sub-region options may eventually work too. But we need to crawl before we walk.

- And second, trucking and State motorists' organisations - who can do a good job of representing consumers - should be brought in to this new allocation process as soon as possible.

They have the competence to do this well: most of them employ former Main Roads officers. But their incentives are different: they are strongly consumer oriented. They work for about 7 million of Australia's most issue-focused consumers.

It may shock those of you from the water sector to know that the consumer organisations are up for this opportunity.

As long as this is not mere consultation, but rather to act as equal partners in deciding which projects are in consumers' interests.

Such a new allocation process is outlined in detail in our 2014 Report.

Since today is not a roads conference, but more about what roads can learn from water, I won't elaborate further.

But from water, roads can draw upon three things:

- User pays is an essential concept for efficient allocation of infrastructure resources.

- A portfolio of solutions to a supply problem, including the option of pricing variations rather than just a never-ending process of spending on new infrastructure should be considered.

- Consumer engagement is going to be vital to making any revised pricing structure work. If people don't understand the choice they are being offered via pricing reforms, they won't buy the change.

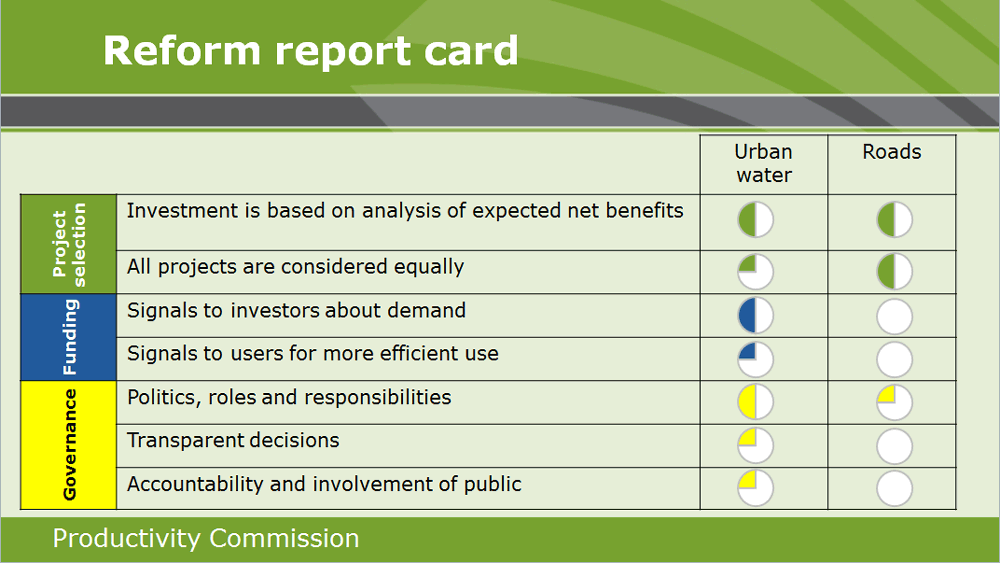

Just to show where each of the two infrastructure providers is up to, in a development sense:

In the model we propose, the private sector might fund some projects, effectively turning an up-front capital cost into a recurrent cost.

To date, we have used tolls on new roads for this purpose.

But charging to use the new, more efficient road while leaving the old roads system as an apparently free good is not necessarily supporting efficient resource allocation.

The desirable productivity outcome is that the most efficient means of distributing goods and workers around a city is used.

This outcome may be defeated because the inefficient road appears unpriced; but the efficient road is priced.

This would be a perverse outcome, created by an unpriced system.

Yet there is no mechanism, until we create the new Commonwealth/State structure, to choose how to address this.

A bit like the earlier discussion on water, as road users you might be asking yourselves if any of this is really likely.

Could governments ever come to accept that pricing a mix of existing and new roads in urban areas is a better way of selecting and paying for roads than the politically attractive, big budget, tax-funded roads announcements of today?

And like water reform, I'm not naïve about this either.

It will take a long time, if it is to happen.

But the first steps are not really too courageous.

They will disturb existing models, to be sure.

But as the slide on expected road investment shows, that disturbance is coming, wanted or not.

And they offer clear benefits to governments, as well as consumers.

For governments, there is the prospect of gaining support that some have struggled to obtain from the community for their big projects - as they fail to explain them effectively, and avoid discussing costs and benefits.

The process we propose instead requires an exposure of costs and benefits to the NRMA or RACQ or similar bodies. These are well-informed critics, open to big investment but wary of pipe dreams. They can help, both to push new ideas but also to kill off silly ones.

And via this we achieve the second benefit: better planning.

And then, after it has all bedded down, the structure is available to move towards user pays, if and when the technology is available.

It will require sustained commitment, to be sure.

But privatisation recycling will only get you so far. If for no other reason than that there is a limit to what a State has available to sell.

And unless tax reform, now under discussion, actually provides additional money not just for education and health but for roads as well, then the options really start to narrow.

And pricing might then actually get a go.

Meantime, there are these early essential steps.

States and Federal authorities should combine their road funding to create a joint fund. As water authorities know, split responsibilities reduce the effectiveness of decision-making.

Consumers need a clear right to be involved in decisions. Roads and Motorists associations should, on behalf of consumers, be given equal rights with roads authorities to consider future major roads investments.

The slate of chosen projects should then be made available to external financiers, to see who is prepared to fund what.

The relevant Ministers will still announce the projects, since at this point and for some time to come they are the parties with the money, and the golden rule always applies: he who has the gold makes the rules.

But if, as the chart on road use suggests, the range of projects exceeds the available funds, then the joint Commonwealth and State funding pool could eventually be mixed with direct user charging. And to make this consumer-acceptable, both State and Commonwealth will need to reduce the call on motorists via registration and excise, as an incentive to make the shift.

The gain, ultimately, is in the link between use and charge.

Something that water users know well.

But road users don't.