Superannuation: Assessing Efficiency and Competitiveness

Draft report

This draft report was released on 29 May 2018.

You were invited to examine the draft report and to make written submissions by 13 July 2018.

The final report was handed to the Government on 21 December 2018 and publicly released on 10 January 2019.

Please note: This draft report is for research purposes only. For final outcomes of this inquiry refer to the inquiry report.

Download the overview

- Overview - Superannuation: Assessing Efficiency and Competitiveness - Draft report (PDF - 1221 Kb)

- Overview - Superannuation: Assessing Efficiency and Competitiveness - Draft report (Word - 1288 Kb)

Download the draft report

- Superannuation: Assessing Efficiency and Competitiveness - Draft report (PDF - 5616 Kb)

- Superannuation: Assessing Efficiency and Competitiveness - Draft report (Word - 5298 Kb)

- At a glance

- Infographic

- Draft supplements

Key points

- Australia’s super system needs to adapt to better meet the needs of a modern workforce and a growing pool of retirees. Currently, structural flaws — unintended multiple accounts and entrenched underperformers — harm a significant number of members, and regressively so.

- Fixing these twin problems could benefit members to the tune of $3.9 billion each year. Even a 55 year old today could gain $61,000 by retirement, and lift the balance for a new job entrant today by $407,000 when they retire in 2064.

- Our unique assessment of the super system reveals mixed performance.

- While some funds consistently achieve high net returns, a significant number of products (including some defaults) underperform markedly, even after adjusting for differences in investment strategy. Most (but not all) underperforming products are in the retail segment.

- Fees remain a significant drain on net returns. Reported fees have trended down on average, driven mainly by administration costs in retail funds falling from a high base.

- A third of accounts (about 10 million) are unintended multiple accounts. These erode members' balances by $2.6 billion a year in unnecessary fees and insurance.

- The system offers products and services that meet most members’ needs, but members lack access to quality, comparable information to help them find the best products.

- Not all members get value out of insurance in super. Many see their retirement balances eroded — often by over $50,000 — by duplicate or unsuitable (even 'zombie') policies.

- Inadequate competition, governance and regulation have led to these outcomes.

- Rivalry between funds in the default segment is superficial, and there are signs of unhealthy competition in the choice segment (including the proliferation of over 40 000 products).

- The default segment outperforms the system on average, but the way members are allocated to default products leaves some exposed to the costly risk of being defaulted into an underperforming fund (eroding over 36 per cent of their super balance by retirement).

- Regulations (and regulators) focus too much on funds rather than members. Subpar data and disclosure inhibit accountability to members and regulators.

- Policy initiatives have chipped away at some of the problems, but more changes are needed.

- A new way of allocating default members to products should make default the exemplar.

- Members should only ever be allocated to a default product once, upon entering the workforce. They should also be empowered to choose their own super product by being provided a 'best in show' shortlist, set by a competitive and independent process.

- An elevated threshold for MySuper authorisation (including an enhanced outcomes test) would look after existing default members, and give those who want to get engaged products they can easily and safely choose from (and compare to others in the market).

- This is superior to other default models — it sidesteps employers and puts decision making back with members in a way that supports them with safer, simpler choice.

- These changes need to be implemented in parallel to other essential improvements.

- Stronger governance rules are needed, especially for board appointments and mergers.

- Funds need to do more to provide insurance that is valuable to members. The industry’s code of practice is a small first step, but must be strengthened and made enforceable.

- Regulators need to become member champions — confidently and effectively policing trustee conduct, and collecting and using more comprehensive and member-relevant data.

Media release

Why our Super system needs to be modernised

'Australia’s $2.6 trillion super system has become an unlucky lottery for many Australian workers and their families. The system is working well for many members, but not for all,' Deputy Chair of the Productivity Commission Karen Chester said on release of the Commission’s draft report Superannuation: Assessing Efficiency and Competitiveness.

The Government tasked the Commission to assess the performance of the super system — to determine if it is meeting the needs of members and retirees and providing the best possible investment returns. And the Commission has today delivered a mixed report card. Too many members are getting subpar returns, at a substantial cost to their income and wellbeing in retirement.

'We have had compulsory super for nearly 30 years, but its architecture is outdated,' Ms Chester said. 'The system suffers from two structural flaws — unintended multiple accounts and entrenched underperformance.'

'With default funds being tied to the employer and not the employee, many members end up with another account every time they change job,' Ms Chester said. A third of accounts (about 10 million) are unintended multiples. The excess fees and insurance premiums paid by members on those accounts amount to $2.6 billion every year.

'These problems are highly regressive in their impact — and they harm young and lower income Australians the most,' Ms Chester said.

Most members are in funds that deliver good investment returns, but millions of members are in funds that persistently underperform — over one in four funds. Over an average member's working life, being stuck in a poor performing default fund can leave them with almost 40 per cent less to spend in retirement.

'Fixing these twin problems of entrenched underperformance and multiple accounts would lift retirement balances for members across the board. Even for a 55 year old today, the difference could be up to $60,000 by the time they retire. And for today’s new workforce entrant, they stand to be $400,000 ahead when they retire in 2064,' Ms Chester said.

'The Commission has proposed a package of changes — focused on delivering for all members — to modernise the system and deliver the best possible returns and products,' said Commissioner Angela MacRae.

Foremost, members should only be defaulted once, when they start working for the first time. The Commission is proposing that they should get to choose from a ‘best in show’ list of high performing funds that have been identified by an independent and expert panel. And existing members should be able to readily switch to these funds.

'All members should be able to engage with their super without being bamboozled. Members today face a confusing proliferation of products, some 40 000 options, and information they don’t understand. It’s hardly surprising that many end up in a bad product,' Ms MacRae said. 'Super needs to be simpler and safer for all Australians.'

Part of the problem is that products are most complex during accumulation and most simple in retirement. 'But what we found is that the reverse is needed for most members,' Ms MacRae said. 'No two retirees are the same, so members need good guidance and advice to navigate retirement. But impartial and affordable advice is hard to find.'

Super funds need to do more to provide insurance that is value for money for all members. 'While many members are getting affordable life insurance through their super, some end up with cover that is manifestly unsuitable, including ‘zombie’ insurance policies they can’t even claim on. And many unknowingly have duplicate insurance policies, which can erode their super balances at retirement by over $50,000,' Ms MacRae said.

'And, as in other parts of the financial system, governance needs to improve — trustees of underperforming funds should be merging with better performing funds. And the best people with the right skills must sit on the boards of super funds,' Ms MacRae said.

'To date, most interest in this inquiry has come from the funds themselves. So we are asking all Australians with super (especially young members) to tell us what they think about our ideas and how to make the super system work better for them,' Ms MacRae said. Click on the draft report at www.pc.gov.au and use the brief comments link.

Formal submissions on all aspects of the draft are also welcome.

Contents

- Preliminaries: Cover, Copyright and publication detail, Opportunity for further comment, Terms of reference, Contents, Abbreviations and Glossary

- Overview - including key points

- Draft findings, recommendation and information requests

- Chapter 1 Setting the scene

- 1.1 How does the super system work?

- 1.2 What is this inquiry doing?

- 1.3 How is this report organised?

- Chapter 2 Investment performance

- 2.1 How is the system being assessed?

- 2.2 How has the system performed?

- 2.3 How have options and asset classes performed?

- 2.4 How have different segments performed

- 2.5 What is the variation in performance within the system and segments

- Chapter 3 Fees and costs

- 3.1 Trends in fees and costs

- 3.2 The impact of MySuper and SuperStream

- 3.3 Costs in the SMSF sector

- 3.4 The relationship between fees and net returns

- Chapter 4 Are members' needs being met?

- 4.1 Do members believe they are being well served?

- 4.2 Is there product proliferation and does it matter?

- 4.3 Are products meeting people’s needs in the transition to retirement?

- 4.4 Variety is needed in the drawdown phase

- 4.5 Innovation and quality improvement in the system

- Chapter 5 Member engagement

- 5.1 How engaged are superannuation members?

- 5.2 Are active members and member intermediaries able to exert material competitive pressure?

- 5.3 Better (not more) information and advice is needed for meaningful engagement

- Chapter 6 Erosion of member balance

- 6.1 Multiple accounts

- 6.2 Delayed and unpaid SG contributions

- 6.3 Undue erosion

- Chapter 7 Market structure, contestability and behaviour

- 7.1 Is the market structure conducive to rivalry?

- 7.2 Is the market contestable at the retail level?

- 7.3 Does vertical integration affect competition in wholesale markets?

- 7.4 Are there unrealised economies in the system?

- Chapter 8 Insurance

- 8.1 A framework for assessment

- 8.2 Some context

- 8.3 How significant is balance erosion?

- 8.4 Do members get value for money?

- 8.5 Recent initiatives fall short of what is needed

- 8.6 Further actions are required — by industry and government

- 8.7 Fiscal effects

- Chapter 9 Fund governance

- 9.1 Fund governance: what is it, why does it matter and why is it regulated?

- 9.2 How do funds perform on board composition and assessment?

- 9.3 How well do funds deal with conflicts of interest?

- 9.4 How do funds rate on transparency?

- 9.5 What is the evidence on funds’ investment governance performance?

- 9.6 What do funds’ merger decisions look like?

- 9.7 Trustee boards’ decisions on uses of members’ money

- 9.8 Overall conclusions on fund governance

- Chapter 10 System governance

- 10.1 System governance is a work in progress

- 10.2 Multiple regulators contribute to system governance

- 10.3 Material systemic risks are not evident

- 10.4 Significant issues lie in data reporting

- 10.5 The level and pace of reform are broadly appropriate

- 10.6 Overall conclusions on system governance

- Chapter 11 Overall assessment

- 11.1 The assessment was not straightforward

- 11.2 Competition is not being fully harnessed

- 11.3 Long term net returns are not being maximised

- 11.4 Members’ needs are not being fully met

- 11.5 Governance has improved, but still falls short

- 11.6 Not all members receive value for money insurance

- 11.7 System performance and member outcomes have improved, but have a way to go

- Chapter 12 Competing for default members

- 12.1 How does the current default system perform?

- 12.2 Foundations for a modern default allocation system

- 12.3 How do alternative default approaches perform?

- 12.4 Preferred approach to the expert panel

- 12.5 The best option for future default arrangements

- 12.6 Some propose a government monopoly provider

- Chapter 13 Modernising the super system to work better for all members

- 13.1 Healthy competition for new default members

- 13.2 A higher standard of performance

- 13.3 Products that meet member needs

- 13.4 Insurance that works for members

- 13.5 Regulators that are member champions

- 13.6 How these improvements will benefit members

- Appendix A Inquiry conduct and participants

- Appendix B Data sources

- Appendix C Surveys: an overview

- References

Cameos

Roadmap to the report

Video: A Better Super System for You

Transcript of video

Our super system has become a lottery – lucky for most people but unlucky for many others.

We’ve got some ideas to make the super system work better for everyone – and we need to make sure young people are put into ONE top performing fund.

It’s hard to get young people interested in their super. And you can’t blame them because today super is more complex than it should be.

But we can make changes so the super system works better for today’s workers and retirees.

In today’s super system, if you don’t choose where your super money goes, your employer does.

And we’ve found that your money isn’t always ending up in the best performing super fund.

A small difference in how your fund performs will make a big difference when you retire.

We think new employees should get to choose from a small list of the top performing super funds, a best in show list, but still be able to pick any fund they want.And if you don’t choose a fund, then your default fund comes from the best in show list.

Once you are put in this fund, it will follow you, across every new job and new employer.

Unless you make a choice to move to another fund.

This will stop your super balance being eaten up by multiple fees and insurance premiums.

In some cases you might be paying premiums for insurance you’re not even eligible to claim on – a zombie insurance policy.

For people who are already paying super we have some ideas on how to get more people into the top performing funds and how to stop people having multiple accounts they don’t want.

Even if you aren’t that young, you can be a lot better off in retirement.

These changes will make it easier for you to find the best performing funds so you can safely decide whether you should stay or move funds.

And so you can also get helpful advice when you get closer to retirement.

We want to hear from you, on what you think about our ideas.

Visit the Productivity Commission website to read the full draft report and its recommendations to improve Australia’s superannuation.

Download the infographic

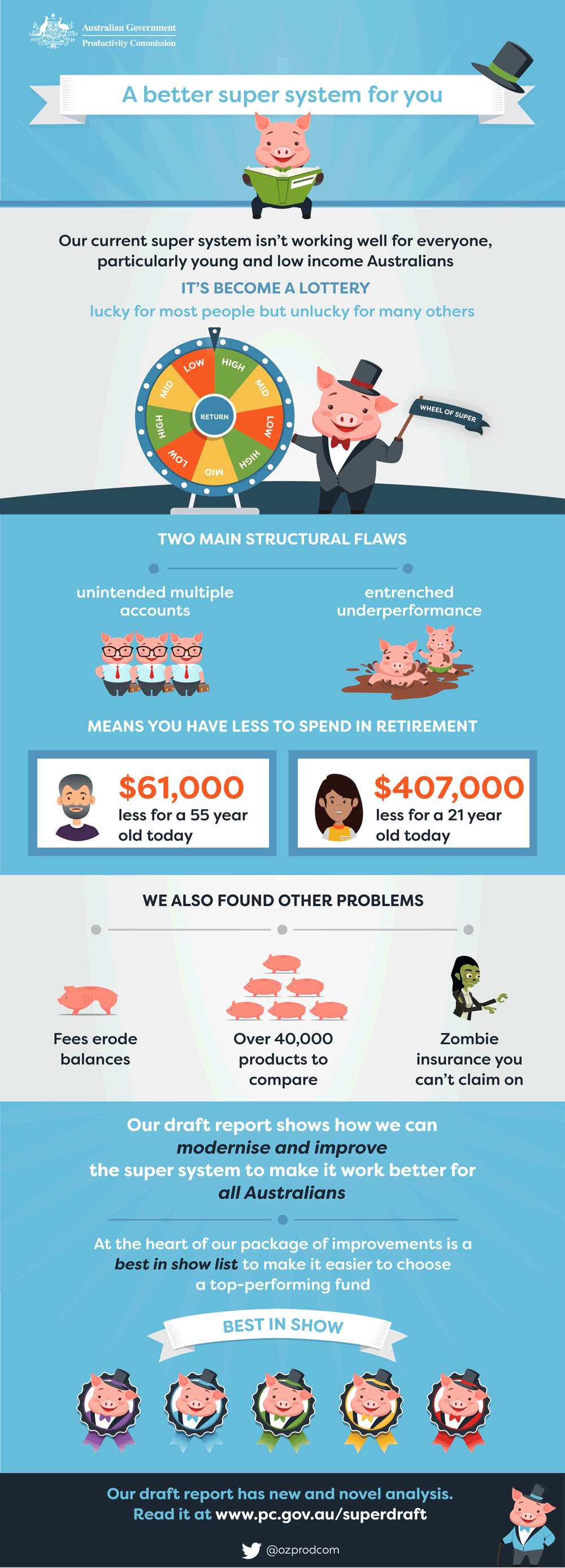

A better super system for you (Text version of infographic)

Our current super system isn’t working well for everyone, particularly young and low income Australians.

It's become a lottery

Lucky for most people but unlucky for many others.

Two main structural flaws

- Unintended multiple accounts

- Entrenched underperformance.

Means you have less to spend in retirement

- $61,000 less for a 55 year old today

- $407,000 less for a 21 year old today.

We also found other problems

- Fees erode balances

- Over 40,000 products to compare

- Zombie insurance you can’t claim on.

Our draft report shows how we can modernise and improve the super system to make it work better for all Australians.

At the heart of our package of improvements is a best in show list to make it easier to choose a top-performing fund.

Our draft report has new and novel analysis. Read it at www.pc.gov.au/superdraft

Supplementary papers

Fiscal impacts of insurance in superannuation

- Fiscal impacts of insurance in superannuation (PDF - 608 Kb)

- Fiscal impacts of insurance in superannuation (Word - 374 Kb)

Investment performance: Supplementary analysis

- Investment performance: Supplementary analysis (PDF - 2542 Kb)

- Investment performance: Supplementary analysis (Word - 5099 Kb)

Economies of scale

- Attachment: External technical peer review by Liana Jacobi (PDF - 207 Kb)

- Attachment: External technical peer review by Liana Jacobi (Word - 21 Kb)

Technical supplements

- Technical supplement 1: Members surveys (PDF - 696 Kb)

- Technical supplement 1: Members surveys (Word - 211 Kb)

- Technical supplement 2: Funds survey (PDF - 526 Kb)

- Technical supplement 2: Funds survey (Word - 179 Kb)

- Technical supplement 3: Governance survey (PDF - 510 Kb)

- Technical supplement 3: Governance survey (Word - 155 Kb)

- Technical supplement 4: Investment performance methodology and analysis (PDF - 1343 Kb)

- Technical supplement 4: Investment performance methodology and analysis (Word - 759 Kb)

- Technical supplement 5: Fees and costs (PDF - 396 Kb)

- Technical supplement 5: Fees and costs (Word - 130 Kb)

- Technical supplement 6: Analysis of members’ needs (PDF - 591 Kb)

- Technical supplement 6: Analysis of members’ needs (Word - 167 Kb)

- Technical supplement 7: Modelling policy changes (PDF - 240 Kb)

- Technical supplement 7: Modelling policy changes (Word - 92 Kb)

Supplementary Funds Survey

- Attachment: External technical peer review by Liana Jacobi (PDF - 207 Kb)

- Attachment: External technical peer review by Liana Jacobi (Word - 21 Kb)

Technical supplements

- Technical supplement 1: Members surveys (PDF - 696 Kb)

- Technical supplement 1: Members surveys (Word - 211 Kb)

- Technical supplement 2: Funds survey (PDF - 526 Kb)

- Technical supplement 2: Funds survey (Word - 179 Kb)

- Technical supplement 3: Governance survey (PDF - 510 Kb)

- Technical supplement 3: Governance survey (Word - 155 Kb)

- Technical supplement 4: Investment performance methodology and analysis (PDF - 1343 Kb)

- Technical supplement 4: Investment performance methodology and analysis (Word - 759 Kb)

- Technical supplement 5: Fees and costs (PDF - 396 Kb)

- Technical supplement 5: Fees and costs (Word - 130 Kb)

- Technical supplement 6: Analysis of members’ needs (PDF - 591 Kb)

- Technical supplement 6: Analysis of members’ needs (Word - 167 Kb)

- Technical supplement 7: Modelling policy changes (PDF - 240 Kb)

- Technical supplement 7: Modelling policy changes (Word - 92 Kb)