Productivity and policy challenges in an environment of pervasive uncertainty

Speech

Peter Harris presented a speech to the Economic and Social Outlook Conference on 20 July 2017 in Melbourne.

Download the speech

Download the presentation slides

- Slides - Productivity and policy challenges in an environment of pervasive uncertainty (PDF - 437 Kb)

- Slides - Productivity and policy challenges in an environment of pervasive uncertainty (PPTX - 639 Kb)

Read the speech

When the organisers met with me to set the agenda for this conference session months ago, it was the first time since I have been in Chairman of the Productivity Commission – four years now - that we could not find a consensus and commit in advance to a topic that represented the outlook, the primary focus of policy challenges in the next year or so.

So we noted down the broad consensus was that things are so uncertain that uncertainty itself is the topic.

My own thought was that by July the fog would lift and the focus would be squarely on one main subject:

- perhaps fiscal, with the domestic Budget process struggling with revenue forecasting and mounting debt

- or perhaps political crisis, with a Commonwealth Government in power by a single seat and an array of domestic challenges, from marriage equality through to energy

- perhaps international, with Trump-led challenges to our region’s traditional reliance on the US relationship, or the rise of populist sentiment breaking open the European borderless model

- or maybe instability in China, under pressure from debt and the ever-rising local expectations generated from what must be the most astonishing economic transformation in human history.

But I was wrong. These were the great uncertainties 12 months ago - and again six months ago - and still today.

None dominate, yet all are ready to spring a nasty surprise and derail what little remains of a narrative about governing for a better tomorrow.

Paul Kelly’s much-respected first book on the Hawke/Keating reform period was titled The End of Certainty.

Viewed today, I think Paul was a couple of decades too early.

Today, certainty is not just at an end, but like Monty Python's famous Norwegian blue, it has:

'Ceased to be, expired and gone to meet its maker, a stiff, bereft of life, it rests in peace. If it hadn't been nailed to its perch, it would be pushing up the daisies.'

…

One of Australia’s more powerful regulators once observed to me that regulators are regularly called upon to deliver certainty, but few businesses realistically can ever expect it.

And we can add employees to that too, as higher demands for skills and automation put an end to concepts like jobs for life.

Yet there is also an important upside to uncertainty.

Opportunity is usually suppressed if certainty is to be assured. And responding to uncertainty increases demand for innovation.

Businesses with powerful regulator protection once could be confident of the future.

But today - desirably for all of us as consumers – such bastions against change look increasingly unsafe from digital disrupters.

In the reform period marked by Paul Kelly’s book and on into the 2000s, some sacred cows remained untroubled by national competition policy and a more open international trading environment.

The celebrated examples were:

- newsagencies

- taxis

- pharmacists

- intellectual property.

Today, digital disruption has done for two of these what reformers could not: ended certainty, and offered an alternative that consumers have made very successful.

Viewed from a national perspective, we are better off, although the transition has not been well managed and policy-makers appeared out of touch. Denial was the principal mode of transition for years in the case of both taxis and newsagencies.

And it appears that technology is now coming for the last remaining bastions.

Should denial again dominate thoughtful transition, this will further reduce the community confidence in the far-sightedness of policy-makers.

…..

This morning, the topic says we should be talking about productivity.

I’d like to repeat that with a little more emphasis: we should all be talking about productivity.

Because in its most important form, this force that has been primarily responsible for lifting incomes and creating value to share amongst labour and capital for decade after decade since the early stages of the Industrial Revolution appears to be in decay across the developed world.

In Australia, some people have celebrated the return of productivity in Australia to about average, after a significant period of underperformance.

Beneficial as an upturn may be, the celebration is premature. The Australian economy has not returned to pre-2004 norms, when productivity first started its decline. Thus the leap to conclude that that structural reform of markets and public services is unnecessary is in fact poorly-founded.

National income growth is down and is not likely to return readily to levels that most of those in this room have experienced over their working lives.

And the assumption that Australia can hold on to its average labour productivity performance in the current policy environment is a brave call.

I will shortly show why, but before I do that I’d like to add the most important caveat of all – that average will simply prove insufficient to keep national income growth healthy.

I define healthy as the trend of income growth that we have all experienced over the past 50 years or so.

When I came into this job four years ago, I made the then dire state of productivity growth – particularly the X factor in productivity, MFP - a theme of my early presentations. These are on our website.

And so as not be considered too alarmist, one scenario I covered was the return of labour productivity to its historical average.

Average was, however, never going to be good enough, and so it has proven.

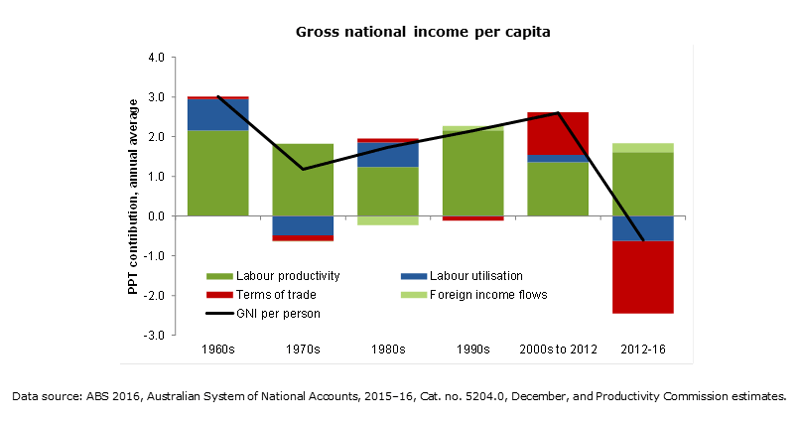

Contributions to income growth

It was evident in 2013 that we would need to outperform in productivity growth in Australia in this decade if we were not to see a slowdown in income growth.

The reason for this is that we have a lot of negative growth influences to offset with our meagre productivity growth.

Aside from the influence of the terms of trade, which is pretty much beyond our control but may be more neutral in future, the outlook for income growth is populated by downward-pointing probabilities:

- demographic declines in workforce participation, with an increasing proportion of the workforce in age cohorts that work less

- technology replacing some jobs that have regular routines, with the prospect of more to come

- literacy and numeracy standards falling for the most part, even though we are investing heavily in the current education system

- the end of jobs for life meaning the loss of the training at the firm level that once accompanied them

- perhaps worst of all, sluggish new capital investment.

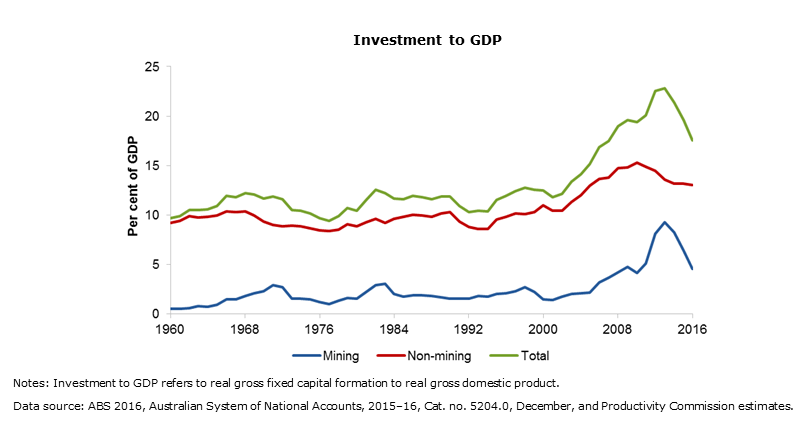

Since the end of the Global Financial Crisis, more than five years now, new fixed capital investment has delivered almost no growth.

This despite the historically low cost of debt, the return of the exchange rate to traditional levels vs the US $, and relatively positive consumer behaviour.

We could perhaps take a relaxed view. One way to take comfort is to note that as a proportion of GDP, investment is about the same as it was a decade ago.

Mining and non-mining investment activity

But its direction is down.

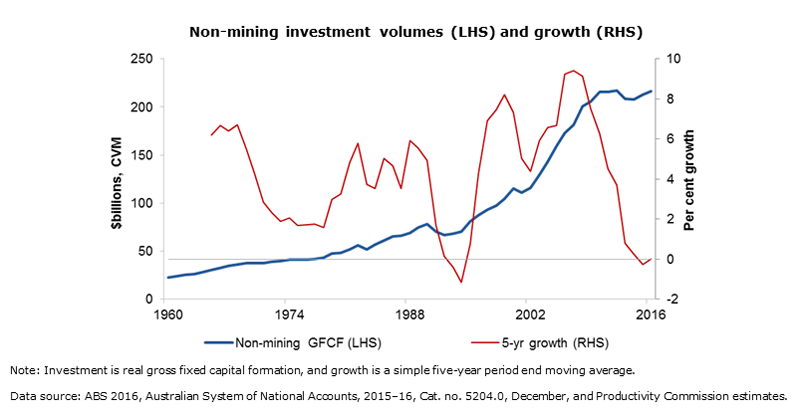

Non-mining investment growth

And we need it to be up if we are to rely on it to support stronger employment growth and shift the demand for labour towards higher wage outcomes.

All the direction signs for these important input factors are down.

And is this unusual? You bet it is. It’s that uncertainty thing again.

…

In the face of this outlook, we need to ensure we are doing all we can in adjusting our economic inputs and regulations to offset these forces.

Where to start…

- A right to return, in education

- A serious spring clean of urban planning

- Address disease prevention as directly as we address workplace accidents

- Change the early retirement paradigm

- Data, the new resource discovery

- Stop creating new barriers to trade and labour mobility.

We could, for example, restructure the approach to education throughout working lives to recognise the multiple careers people are likely to have, and make it simple and cheap to return to education. A right to return is no bad thing for an uncertain future. Retraining is currently inconvenient and expensive, and our key educational institutions are still emphasising a one-career-for-life approach to qualifications. The system – both in terms of education and industrial relations - is set up against becoming a plumber at age 30, or a chef at age 40.

Or we could take the serious broom to the accrued debris of decades of unreformed investment-sapping limitations in planning and zoning and urban infrastructure costs. I suggested how to the last Outlook Conference.

Maybe we could take a direct approach to a healthier workforce, move away from fee-based responses to disease and redirect funding towards prevention. We could use agents who make it their primary business to prevent performance-reducing disease. We do this now for accident prevention, but not for diabetes or drugs.

We could apply a whole-of-government data-based attack on employer expectations of early retirement, along with re-framing the age of access to our superannuation and pension systems. We are living longer, but our working lives have barely increased at all in forty years. Someone is paying for that, and despite the view that we are putting lots into our superannuation, it’s not offsetting those extra years in retirement. Indexing both of the access ages to future improvements in longevity has an unmistakable logic, and depoliticises the whole thing.

And we need to open up the use of data more generally, as one of the very few perpetually renewable resources discovered this century.

Plus renewing effort at the removal of barriers to efficient resource allocation: eliminating non-tariff barriers, shifting the tax mix to allow greater labour mobility are good starts.

But we aren’t even close to doing any of that.

..

Shortly, we will complete the first Report to the Treasurer in a new series, to be repeated every five years, on how to shift the dial in productivity.

This Report will not accept as a plan that average rates of productivity growth are good enough.

It will analyse just how far we can expect productivity growth to retreat in the presence of the factors I’ve outlined, and a passive policy response.

The analysis will also recognise the current uncertainty and argue for it to be embraced.

Denial is not a policy.

The likes of Uber or Alipay or Amazon or Tesla or Google are not threats to incumbent firms because of their algorithms, much though the fear of artificial intelligence is rising. They are threats because they are popular, cheaper, more effective.

Giving regulators permission to experiment – something that wasn’t done well with Uber and taxis but is now being given better forethought in fintech - is a genuinely important contribution by governments.

Another is getting serious about communication.

Too often, our leaders – from all political persuasions - wait and wait, and fail to authorise actions in support of effective adaptation.

Or worse still, play to the gallery and jam in the wedge.

Credibility is a precious commodity. A stock of it is created by persistently offering simple, clear advice that recognises a policy shift is on, and explains why – and where the national interest lies.

It is a real pity to see credibility eroded so often by defaulting instead to offering false hope or railing against the inevitable.

….

The offering of false hope is not limited to Australia.

A specific example is the global steel industry. Around the developed world, wishful sentiment is translating into unrealistic expectations of protection.

There is a long history of this industry demanding and receiving significant levels of protection, with two outcomes now probable.

First, a sudden return to profitability that is dependent on protection rather than fundamentals makes support exceptionally hard to remove, even when (say) dumping ceases.

Second, the punishment of local industries which use steel as an input by leveraging a spike in price to become a permanent increase (30% to 60% above long term average in Australia today).

The steel industry is fast becoming a severe test of the rigour with which Australia approaches inherently manipulable policies like anti-dumping.

The scenario internationally is one where the US and Europe apply what one Australian steel executive reportedly described as anti-dumping on steroids.

More US protection is already planned, we are confidently told, but Australia is exempted from it.

That is hardly a relief for the Australian economy as a whole.

For East Asian steel producers - often using our iron ore - significant destabilisation of traditional markets is likely. Supply will chase after less protected locations. With big volumes potentially in play, the international market-clearing price falls, and our producers will seek to again be protected from the consequences.

To the extent our steel sector wins that, our construction, housing and infrastructure sectors lose.

This is the contagion that occurs when neo protectionism is set free.

…

Worse still, we now face this on a global scale, rather than just in the handful of markets long known for their highly protected nature.

With the election of President Trump, US trade policy now features a number of explicitly protectionist commitments, some of which have the capacity to trigger serious international economic disruption, including for Australia.

Based on our long history of rigorous advice to the Australian Government on trade policy, the Commission commenced work in January on an analysis of core elements of the new US policy.

Some may be sanguine about this development. After all, many countries today seek to use trade negotiations simply to advantage their export industries, with inattention or even hostility to imports, despite the harm to their economies and populations as a whole.

Yet even in realpolitik terms, the new US trade policy is radically different to that which has prevailed for decades.

And since so many nations count the US as a key trading partner, it has clear global ramifications.

We modelled a number of scenarios. The core examples, drawn from various statements, are:

- the US imposes tariffs of the order of 35% or 45% on China and Mexico

- the US applies a Border Adjustment Tax, equivalent to a 20% tax on imports and a 20% subsidy on exports

- a tit for tat response to protectionist actions results in a trade war, with average tariff increases of 15 percentage points globally.

The results of this analysis were insightful.

Large US tariff increases on Mexico and China do not improve the overall US trade deficit. They instead stand to reduce US growth - by a little less than half its current rate.

The damage to the Chinese economy would be of the same order of magnitude in GDP growth terms. But the impact on Mexico would much graver.

The impact on Australia would be minimal, other than the chilling effect of uncertainty. But this is hardly a comfort, as uncertainty – the topic of today’s panel – is rampant already.

Our analysis of the Border Adjustment Tax concept suggests that, again, uncertainty is likely to be the bigger factor in any Australian impact, although specific Australian exporters to the US can be expected to vociferously call for the Government to seek another special deal should the tax apply.

The worst case scenario is an outbreak of global tariff increases.

The modelling suggests a global recession is a genuine potential consequence should the sentiment that drives the new US approach become a global sentiment. China first, Europe first, Russia first, Australia first – it isn’t possible, of course, but the consequences are likely to be ugly for all.

The implications for Australia are bleakest under this scenario.

If we were to participate in a general raising of tariffs to 15% – a strong temptation for poorly-informed politicians to compete over – our estimates show:

- the average household would end up $1500 per year worse off

- in employment terms, we would have 100 000 fewer jobs

- up to 5% of Australian capital stock would be mothballed or close in perpetuity.

This is a modelled scenario and the Productivity Commission is very conscious of the limits of modelling.

We use them to illustrate the direction of impact, and there can always be debate about the precision of numbers.

What is not debatable in any serious way is the adverse direction of the data.

For the Australian Government, the advice of the Productivity Commission is clear and specific: don’t participate, if it comes to this truly sad place.

Instead, recognise and argue that we can demonstrate as a nation the benefits of unilateral reductions in protectionism and a solid commitment to redistribution of income across the income cohorts.

And here is an irony not obvious to me until I took on this job: while in Australia structural reform today struggles to hold the political respect with which it was once viewed, offshore the respect for the ‘Australian model’ as they called it in South America and South Asia grows.

We have walked the talk of reform in the past, and lifted ourselves from the prospect of being the poor white trash of Asia to being an exemplar.

We can show to our citizens that getting off the never-ending pathway of protecting this, subsidising that, and countervailing anything in between has been extraordinarily beneficial to this nation as a whole.

Yes, we can also improve our redistribution policies so that those who face adjustment are supported, particularly if we apply retraining and labour mobility reform as I mentioned earlier.

But this conditional comment does not reduce the clarity of the outcome.

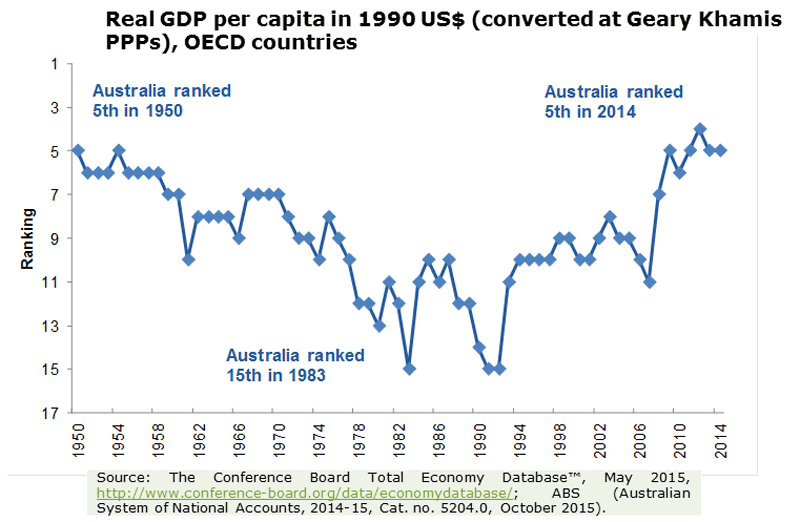

Taken over my lifetime, Australia has moved from amongst the world’s wealthiest nations, to one of the poorest performers of the developed world, and now back up again.

Australia’s OECD economic ranking

And we should be in no doubt, in considering how to respond to global moves towards protection, trade matters a great deal to the Australian economy.

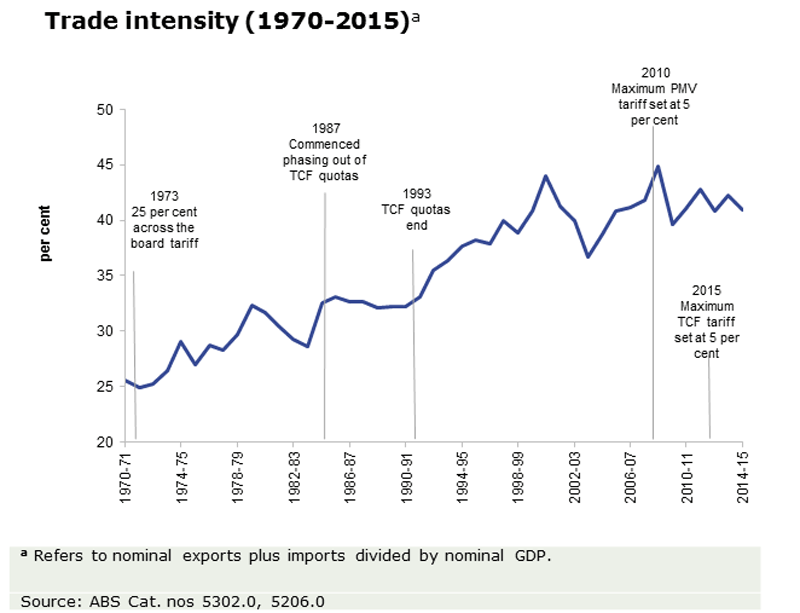

A more open economy

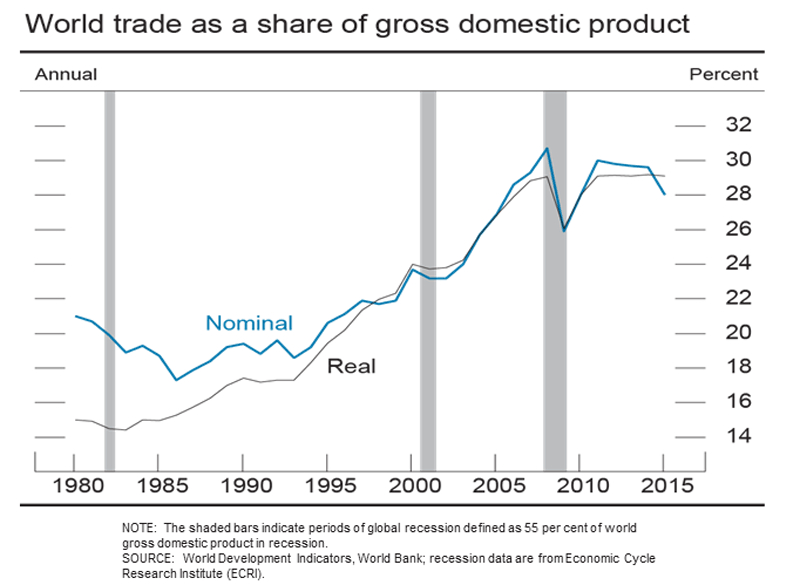

At the global level, trade is stalling. The US Federal Reserve published this last week.

This, one of the primary means of lifting nations out of poverty and yet benefiting us in the developed world too.

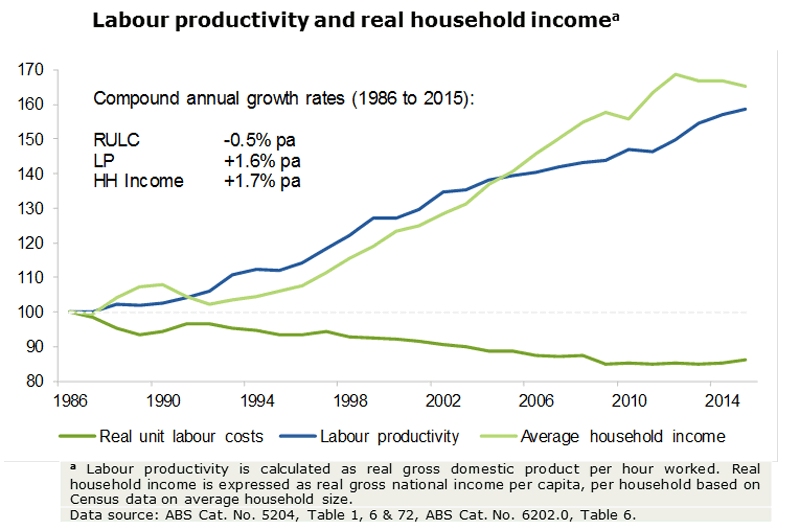

For Australia, the net result looks like this: unit labour costs slowly fall, encouraging employment; but household incomes rise due to social redistribution policies, eventually exceeding productivity growth over a sustained period.

Household income has improved significantly

Still, we can do better than that.

And later this year, our 5 Year Productivity Review will offer more detail on specific reforms; and the engagement with States and Territories that will be essential to that.

We need to shift the productivity dial, to ensure that incomes can continue to rise in a manner that makes most people more confident rather than less confident about the direction of public policy.

Meantime, in a world of uncertainty we can still be certain of one thing: an open economy benefits Australia, and the temptation to ape poor public policy offshore should be resisted.