PC productivity update 2015

ISSN 2202-7378

This publication was released on 20 July 2015 and in this edition the Commission analyses the latest ABS productivity statistics and comments on new developments underlying Australia's recent productivity performance.

Each edition will unpack the latest ABS productivity statistics, and report on the findings of the Commission's most recent research into productivity issues.

Download the update

Productivity At A Glance

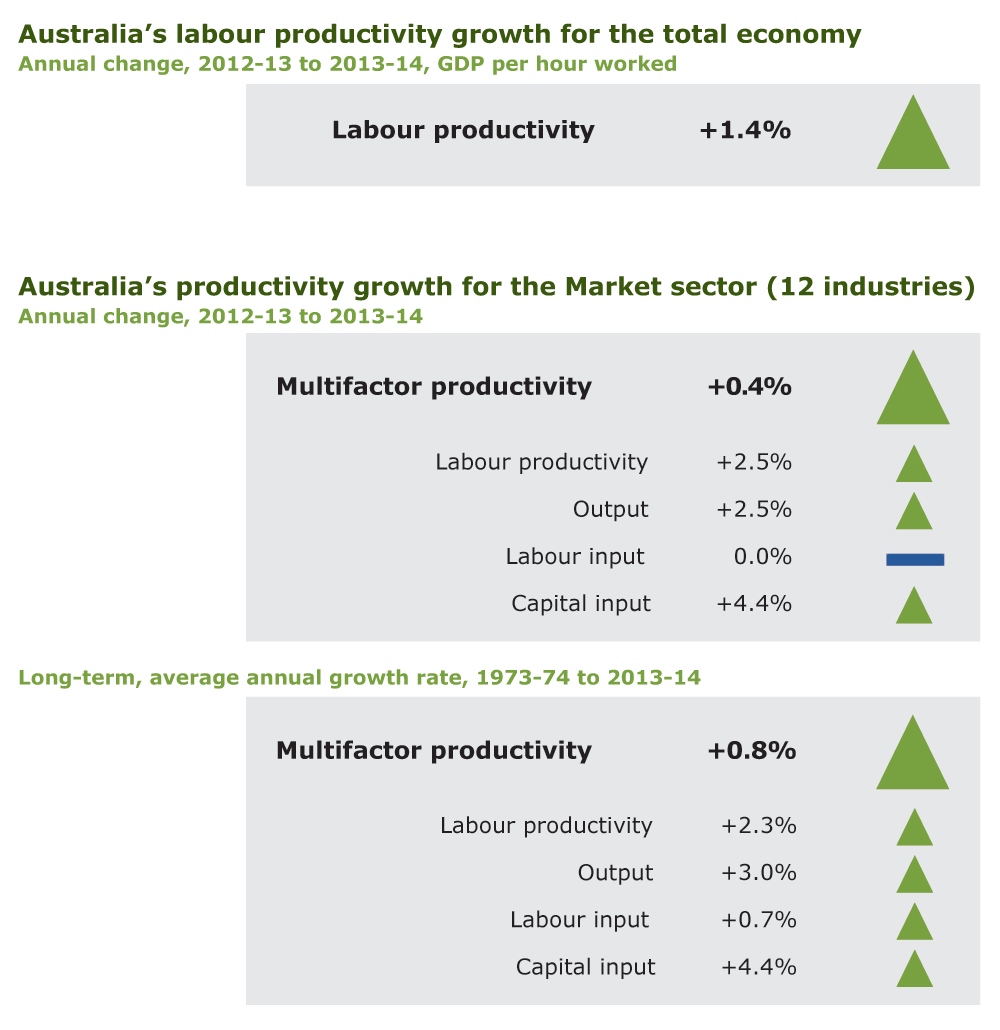

Australia's labour productivity growth for the total economy (Text version of above image)

Annual change, 2012-13 to 2013-14, GDP per hour worked

Labour productivity +1.4%

Australia's productivity growth for the Market sector (12 industries)

Annual change, 2012-13 to 2013-14

Multifactor productivity +0.4%

Labour productivity +2.5%

Output +2.5%

Labour input +0.0%

Capital input +4.4%

Long-term, average annual growth rate, 1973-74 to 2013-14

Multifactor productivity +0.8%

Labour productivity +2.3%

Output +3.0%

Labour input +0.7%

Capital input +4.4%

Data sources: ABS (Australian System of National Accounts, 2013-14, Cat. no. 5204.0, November 2014); ABS (Estimates of Industry Multifactor Productivity, 2013-14, Cat. no. 5260.0.55.002, December 2014).

For more detailed productivity statistics and commentary see Chapter 1.

Printed copies